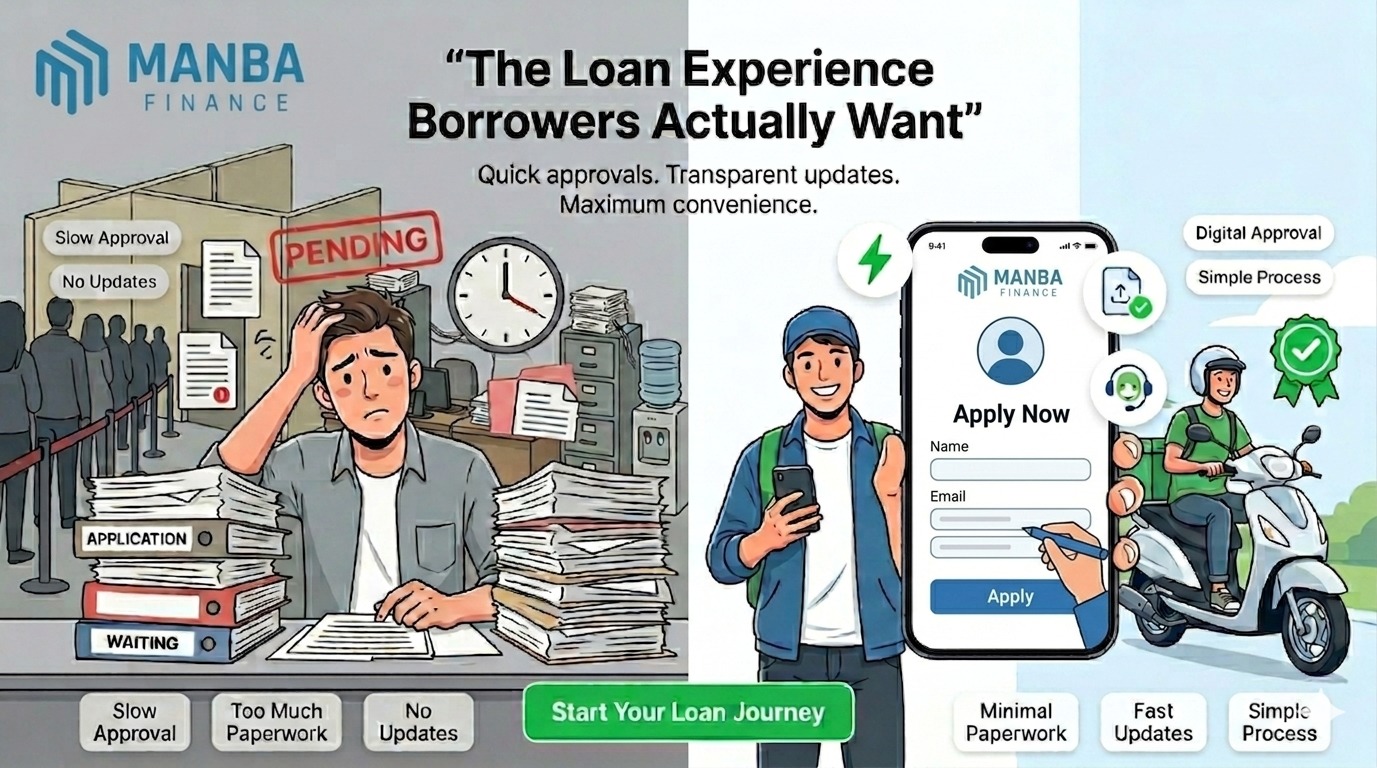

Speed, transparency, and simple documentation beat interest rates when it comes to borrower satisfaction. In 2026, NBFCs will outscore traditional banks on all three not because they’re offering cheaper money, but because applying with them doesn’t feel like a test of patience.

Nobody talks about a loan they got. They talk about the experience of getting it.

“I applied on a Saturday evening and had an update by Monday morning.” That’s the kind of thing people mention when they recommend a lender to a friend or a cousin looking to buy a bike. Not the interest rate. Not the tenure options. The fact that it didn’t feel like pulling teeth.

This shift from product to experience has quietly become the defining battle in two-wheeler financing in India. And if you’re a borrower trying to figure out who to go with, understanding what actually drives satisfaction (and what kills it) will save you a lot of frustration.

Why Borrower Expectations Are Higher Than They’ve Ever Been

Think about what else you do on your phone. You order groceries and they arrive in 20 minutes. You book a flight and get confirmation instantly. You raise a complaint with an e-commerce platform and get a resolution within hours.

That’s the baseline borrowers are working from now. When someone opens a loan application on their phone and hits a wall, an unclear form, a requirement to visit a branch, a “we’ll get back to you” response with no timeline, they’re not just mildly inconvenienced. They’re comparing it to every other digital experience in their life, and the contrast is jarring.

This is especially true for borrowers under 35, first-time applicants, and gig workers who live digitally and have little tolerance for processes that were clearly designed for a different era.

What they expect isn’t extraordinary. It’s just:

– An answer within a reasonable time. Not 7–10 working days. If a decision can’t be given immediately, at least tell them where things stand. That alone reduces anxiety significantly.

– Documents that make sense. Aadhaar, PAN, a bank statement. Not a list of twelve items with asterisks and footnotes about which ones need to be self-attested and which need originals.

– Terms that are stated plainly. What’s the EMI? What’s the total repayment? Are there processing fees? Is there a prepayment penalty? Before signing, not in the fine print after.

– A process that actually works on mobile. This should go without saying in 2026. But some lenders still require desktop browsers, PDF submissions, or physical visits for steps that have been digitally solvable for years.

– Support that actually helps. Not a scripted response. Not a ticket number followed by silence. An actual answer to the actual question.

The lenders doing well on customer satisfaction right now aren’t the ones with the lowest interest rates. They’re the ones who’ve built their process around the borrower instead of around their own operations.

The Five Things That Make or Break the Experience

1. Speed of Approval

This one tops nearly every survey on borrower satisfaction, and the reasons are obvious once you think about them from the borrower’s side.

When someone applies for a bike loan, there’s usually a specific reason. They need the bike for work. They’ve spotted a deal at a dealership. They have a window before prices go up. A loan decision that takes ten days doesn’t just feel slow it may actually cause them to miss what they were planning for.

More than that: waiting with no information is genuinely stressful. Borrowers who get a decision within 24–48 hours rate their experience significantly higher even when other parts of the process weren’t perfect simply because the wait didn’t drag them through uncertainty.

NBFCs have a real edge here. They’re not running applications through multiple layers of manual approval built for a time when that was the only option. Automated eligibility checks, digital document verification, faster internal workflows the result is decisions that come back in days or sometimes hours, not weeks.

2. Documentation

Ask any first-time loan applicant to describe their biggest stress point. Most of them will say paperwork not because they don’t have the documents, but because they’re never quite sure if what they’ve submitted is enough. Or in the right format. Or whether that one missing thing is going to restart the whole process.

The lenders who score well on this are the ones who’ve been ruthless about cutting requirements down to the essentials. Aadhaar for identity. PAN for tax records. A few months of bank statements for income. Phone photos uploaded through an app. Done.

Every extra document you ask someone to produce is friction. And friction, at scale, becomes the main reason borrowers choose someone else.

3. Transparency About What They’re Actually Agreeing To

This is where trust either gets built or quietly destroyed.

It’s not usually that lenders lie about charges. The charges weren’t mentioned until later a processing fee that appeared on the disbursement statement, a prepayment penalty buried in clause 14(b) of the agreement, a rate that was “subject to eligibility” and came in higher than what was advertised.

None of these individually are catastrophic. But they create a feeling of having been managed rather than informed. And that feeling sticks.

The lenders borrowers consistently rate highest are the ones who tell them everything upfront what the EMI will be, what fees exist, what the total cost of the loan actually is before asking for a signature. That’s not above and beyond. That’s just honest.

4. The Digital Experience

Mobile-first isn’t a feature differentiator anymore it’s table stakes. But there’s a difference between a lender who has an app and a lender whose digital process is genuinely frictionless.

Real-time status updates matter more than most lenders realise. Being able to open an app and see “Documents verified loan processing” instead of calling the branch and being told “it’s in process” is a fundamentally different experience. One creates confidence. The other creates anxiety.

Lenders still asking borrowers to visit a branch for steps that have been digitally solvable for years are losing applicants who simply move on to someone who doesn’t make them do that.

5. Customer Support

Support quality rarely gets attention until something goes wrong. And then it gets all the attention.

The thing that turns a manageable problem into a lasting bad impression isn’t usually the problem itself, it’s being unable to get anyone to actually help. Being transferred three times. Getting a response that clearly didn’t address what was asked. Being told “someone will call you back” and then waiting.

Lenders who’ve invested in genuinely responsive support teams, people who know the product, have access to account information, and can actually resolve issues rather than log them show up consistently better in customer ratings. Not because problems don’t happen, but because they get fixed.

Banks vs NBFCs: What the Experience Actually Looks Like

| What Matters to Borrowers | Traditional Banks | NBFCs in 2026 |

| Approval speed | 5–14 days, typically | 24–48 hours in most cases |

| Documents required | More extensive, often physical copies | Minimal digital uploads work |

| Eligibility criteria | Credit-score heavy, stricter for non-salaried | More adaptive to actual income |

| Mobile experience | Improving, but patchy | Built for mobile from the start |

| First-time borrower support | Limited built for established profiles | Considerably better |

| How clear the terms are | Variable | Generally clearer with digital-first lenders |

Banks can still offer competitive interest rates. But if you’re a first-time borrower, a gig worker, or someone without a long credit history, the experience of applying to a bank often involves more friction, more rejection risk, and a process that wasn’t really designed with you in mind.

NBFCs didn’t build their processes by digitising legacy systems. They built from scratch which is why the result feels different.

Who Gets Left Behind by Traditional Lending (And Who Doesn’t Have To)

The profile of a “good borrower” in the traditional banking system is pretty narrow: salaried employee, multi-year credit history, clean CIBIL score, complete documentation. If you tick all those boxes, any lender will take your application seriously.

But a significant portion of people who need and can afford bike loans don’t fit that template.

– Delivery partners and gig workers earn real money often more consistently than many salaried employees but their income shows up in app payouts rather than salary slips. Traditional assessment systems don’t know what to do with that. Digital NBFCs that look at banking patterns and income regularity over time handle these profiles much better.

– Young first-time borrowers haven’t had time to build credit history. A thin CIBIL file doesn’t mean financial irresponsibility, it means they haven’t borrowed before. Lenders willing to look beyond the score and assess actual repayment capacity give these borrowers a fair shot.

– Borrowers outside major cities used to be limited by geography who had a branch near enough to be practical. That constraint is largely gone now. But it only disappears if the digital process actually works end-to-end, which not every lender has managed.

The Complaints That Actually Appear in Reviews

Reading through borrower feedback on bike loans across India in 2026, the same issues come up repeatedly. None of them are about interest rates.

1. Radio silence during the process. Applying and then hearing nothing for days, no update, no request for more information, no acknowledgment that the application exists is the most common complaint by a wide margin. The wait itself isn’t the problem. The silence is.

2. A charge that wasn’t mentioned earlier. Doesn’t matter if it’s ₹500 or ₹5,000. The feeling of discovering a fee that wasn’t disclosed upfront is the same. Borrowers feel like they were managed, not informed.

3. Being asked for the same document again. It signals internal disorganisation and wastes the borrower’s time. It’s also a trust problem if they lost a document you already submitted, what else are they being careless about?

4. Support that couldn’t actually help. Getting bounced between departments, receiving responses that don’t address the question, being promised a callback that never comes. These interactions are small in isolation. Collectively, they define what a borrower says about a lender when someone asks.

5. Terms that weren’t explained before signing. Fine print exists everywhere. But borrowers who feel they didn’t understand what they were agreeing to before they agreed to it are not repeat customers. And they do tell people.

What to Actually Check Before You Apply

Most borrowers spend their research time comparing interest rates. That’s useful but incomplete. A few things worth checking that most people skip:

Look at recent reviews on Google Maps and the lender’s app store listing. Not the testimonials on their own website. Look specifically for patterns in negative reviews. What are people repeatedly complaining about? That’s far more informative than the star rating.

Ask the lender directly: how long does approval typically take for a complete application? A confident, specific answer is a good sign. “It depends” or “usually a few days” is not.

Try using their website or app before you actually need to. Is the application form clear? Is there a status tracker? Is it easy to find contact information? A clunky digital experience at this stage is a preview.

Ask about fees before you get to the final step. Processing fees, documentation charges, prepayment penalties these should all be answered clearly and promptly. A lender who gets vague about fees when you ask directly is a lender worth being cautious about.

Check that they’re RBI-registered. Two minutes on the RBI website. Immediately filters out the bad actors.

Why Manba Finance Works for Borrowers Who Don’t Fit the Usual Template

Manba Finance has processed loans for over 900,000 customers across India and a meaningful portion of them are people traditional lenders would have found reasons to decline or delay.

The eligibility assessment focuses on actual repayment ability rather than just what a credit score says. That matters for first-time borrowers who haven’t had the chance to build a credit history. It matters for gig workers whose income is real but doesn’t sit in a salary slip. It matters for anyone whose financial life doesn’t map neatly onto the profile that banks designed their systems around.

The process is digital, the documentation requirements are straightforward, and the dealer network means the loan-to-delivery experience is coordinated rather than fragmented. That coordination lender and dealership on the same page is something borrowers notice even when they can’t quite articulate why things went smoothly.

Frequently Asked Questions

1. What do borrowers care most about in a bike loan provider today? Speed and transparency, consistently. Interest rates matter, but borrowers who have a fast, clear, low-friction experience rate their lender significantly higher than those who got a slightly lower rate but a frustrating process.

2. Why are NBFCs pulling ahead of banks in borrower satisfaction for two-wheeler loans? Partly structural NBFCs built digital processes from scratch rather than retrofitting legacy systems. Partly flexibility they assess eligibility differently, which means more borrowers get approved without the back-and-forth. Partly speed without multi-layer approval hierarchies, decisions come back faster.

3. Does the mobile experience really affect satisfaction that much? Yes. For borrowers under 35, a loan process that doesn’t work properly on mobile isn’t a minor inconvenience, it’s a dealbreaker. Real-time status updates in particular have an outsized effect on how borrowers feel during the waiting period.

4. What’s the single most common complaint in bike loan experiences? Lack of communication during the process. Borrowers can handle waiting. What they struggle with is waiting without knowing what’s happening or why.

5. How do I pick the right lender? Check recent reviews for patterns, not averages. Ask about fees before the final stage. Test the digital process. Ask for an honest timeline on approval. Verify RBI registration. And weight the experience factors alongside the rate, the cheapest loan with the worst process often ends up costing more in time and stress than it saves in rupees.

The Honest Summary

Getting a two-wheeler loan in 2026 is not complicated. What’s complicated is finding a lender who treats it that way.

The lenders winning on satisfaction right now are the ones who made the process as straightforward as they could: fast decisions, clear terms, simple documents, support that actually helps. Not because it’s a marketing strategy. Because borrowers who have that experience come back and bring people with them.

The ones losing ground are still asking borrowers to adapt to systems that were built for the lender’s convenience, not theirs.

Check your eligibility at manbafinance.com and see what the difference actually feels like.