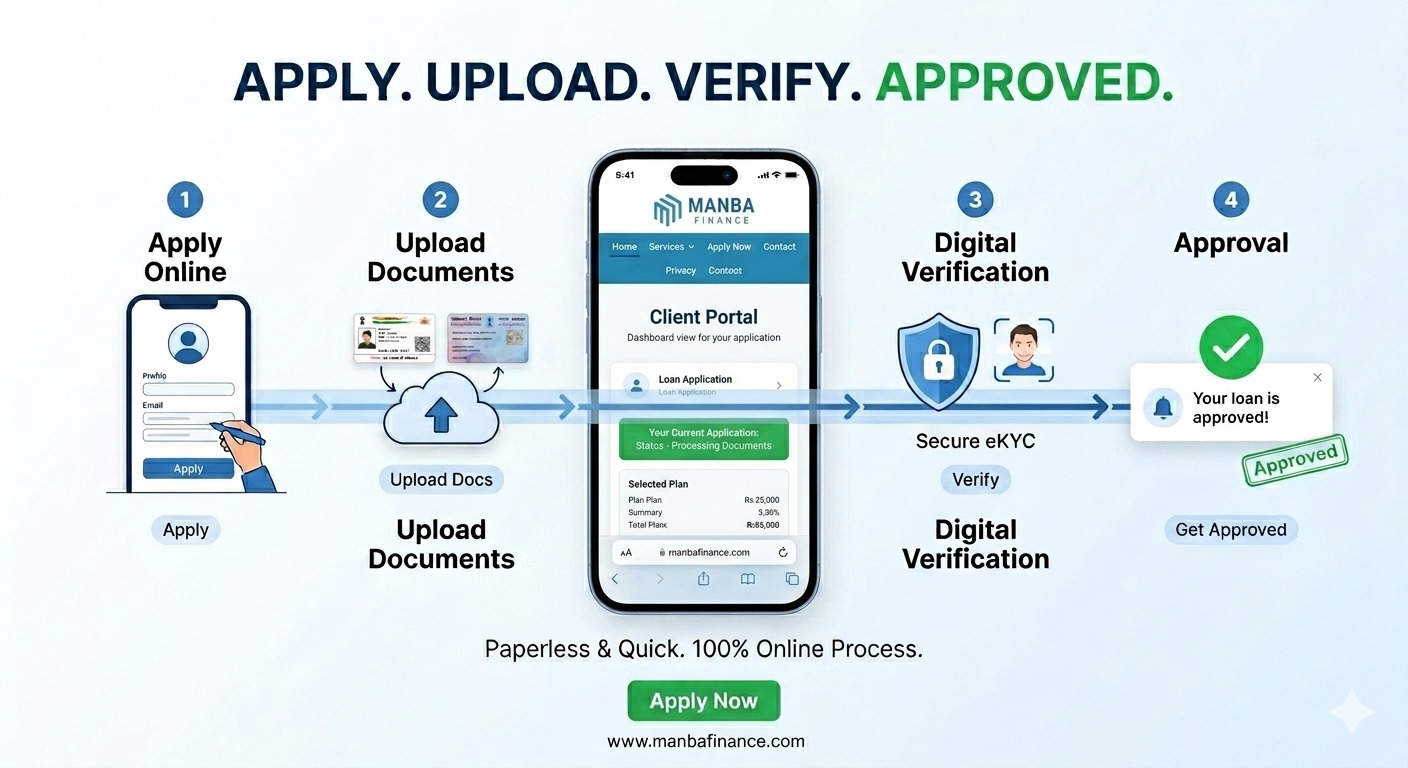

A digital loan approval process lets you apply for a loan, upload documents, complete verification, and receive approval entirely online, without visiting a branch. In 2026, most established lenders in India complete the core steps within 24–48 hours using automated checks, Aadhaar-based eKYC, and real-time status updates.

Most people still think getting a loan means taking half a day off work, carrying a folder of photocopies, and waiting in a queue only to be told to come back with one more document.

That experience is largely gone now. And if you haven’t applied for a loan digitally yet, what’s changed in the last few years would genuinely surprise you.

This isn’t just about doing paperwork on a screen instead of paper. The entire logic of how lenders assess you, communicate with you, and process your application has been rebuilt from scratch. Here’s what that actually looks like in practice and what it means for you as a borrower.

What “Digital Loan Approval” Actually Means

At its core, a digital loan approval process moves every major step online:

- You apply through a website or app no physical form needed

- Documents are uploaded as photos or PDFs no photocopies, no couriers

- Identity verification happens through Aadhaar-based eKYCno in-person checks

- Eligibility is assessed through automated systems not waiting for a manual reviewer to get to your file

- You get status updates in real time calling the branch to find out what’s happening

The result is a process that used to take 7–14 days and multiple visits now often wraps up in 24–48 hours, sometimes faster for straightforward applications.

What Changed And Why It Took This Long

For a long time, lending was paper-heavy by necessity. Lenders needed physical signatures, wet-ink verification, and in-person checks because there was no trusted way to verify identity or income digitally at scale.

That changed when three things came together in India:

- Aadhaar-linked eKYC gave lenders a government-backed way to verify identity instantly, without a person being physically present.

- Account Aggregator frameworks allowed lenders to access bank statement data directly with the borrower’s consent removing the need to submit six months of printed statements.

- Automated credit assessment tools could analyse income patterns, repayment behaviour, and financial stability far faster than a human reviewer going through documents manually.

When all three became widely available, the traditional process didn’t just get faster it became a different thing entirely.

| What Lending Looked Like Before | What It Looks Like in 2026 |

| Physical branch visits (often 2–3) | Fully remote, apply from your phone |

| Printed documents and photocopies | Digital uploads in minutes |

| Manual review 7 to 14 days | Automated checks often 24 – 48 hours |

| Limited to working hours | Apply any time, any day |

| Opaque process with no updates | Real-time status tracking |

| Geography-limited access | Anyone with internet can apply |

The Six Things Digital Platforms Actually Do Differently

1. Application takes minutes, not days

You’re no longer filling out long paper forms in a branch and waiting for someone to enter your data into a system. Online application forms are designed to take 10–15 minutes on a smartphone. The data goes directly into the lender’s system, no transcription delays, no data entry errors.

2. Document submission is genuinely paperless

A clear phone photo of your Aadhaar card, PAN, and bank statement is all most lenders need now. No couriers. No photocopies. No “please submit originals for verification at the branch.”

3. Eligibility assessment is smarter, not just faster

This is the part most people don’t realise has changed. Modern digital platforms don’t just check whether you have a salary slip; they look at income patterns, banking behaviour, and repayment consistency over time. This matters most for gig workers, freelancers, and self-employed individuals who have income but don’t fit the traditional salaried profile that older assessment systems were built around.

4. You can track exactly where your application stands

One of the most frustrating parts of traditional lending was the black box you submitted documents and then just waited, with no idea whether anything was happening. Digital platforms show you exactly where in the process your application is, in real time. No more calling the branch and being told “it’s under review.”

5. Access is no longer tied to geography

If you live in a tier-2 or tier-3 city without a nearby branch of your preferred lender, that used to be a real problem. Digital lending removes that constraint entirely. The process is the same whether you’re in Mumbai or a smaller town in Maharashtra.

6. Communication is faster and more transparent

Approvals, rejections, requests for additional information all come through faster, often via SMS or app notification, with clear explanations rather than vague responses.

Who Benefits Most from Digital Lending

Digital loan processes aren’t just more convenient for everyone they genuinely open doors that were previously closed for specific groups:

1. First-time borrowers: who find the traditional process intimidating, lengthy forms, complicated terminology, and multiple visitors find that guided digital applications are significantly less daunting. The process walks you through each step rather than assuming you already know how it works.

2. Gig workers and self-employed individuals: whose income doesn’t show up neatly on a salary slip. Digital assessment tools that look at banking patterns and income behaviour are better equipped to evaluate these profiles than older systems built around salaried employment.

3. Busy urban professionals: who simply can’t take time off work to visit a branch multiple times. Being able to apply in the evening from your phone, upload documents the next morning, and receive an update the same afternoon fits how people actually live now.

4. Borrowers in smaller cities: who previously had limited access to lenders with good terms because their nearest branch was hours away.

Is It Actually Safe?

This is a fair concern, and it deserves a straight answer: yes, established digital lenders use secure, regulated systems. The more relevant question is how to tell the difference between a legitimate lender and one you shouldn’t trust.

A few simple rules:

- Always apply through the lender’s official website search for the company directly, don’t click links from WhatsApp or unknown SMS messages

- No legitimate lender will ask for your OTP ever. An OTP is a one-time password meant only for you. If someone calls and asks for it, that’s fraud

- Verify the lender is registered with the RBIthis is publicly checkable and takes two minutes

- If something feels off, it probably is legitimate lenders don’t pressure you to apply immediately or offer terms that sound implausibly good

Established NBFCs and banks operating in India’s regulated lending space use encrypted data handling, Aadhaar-based identity authentication, and compliance frameworks that protect borrower data. The technology is safethe risk is in fake platforms impersonating real lenders.

Where Digital Lending Is Headed

The changes so far have mostly been about convenience and speed. What’s coming next is about personalisation and intelligence.

– AI-driven eligibility assessment will move beyond credit scores and bank statements to build a more complete picture of a borrower’s financial reality helping people who are creditworthy but underserved by current metrics.

– Instant eligibility decisions are already available for some loan types and will become standard across most categories.

– Smarter fraud detection means fewer false rejections and faster processing for genuine applicants.

– Fully app-based loan journeys from first enquiry to disbursement without ever needing to switch to a different channel or speak to someone unless you want to.

The direction is clear: borrowing will continue to get faster, more personalised, and more accessible. The gap between applying for a loan and actually receiving it will keep shrinking.

How Manba Finance Fits Into This

Manba Finance built its loan process around exactly the kind of borrower that traditional lending often overlooked first-time applicants, gig workers, salaried individuals with limited credit history.

The application is fully digital: visit manbafinance.com, fill in your details, upload your documents, and track your approval. No branch visits required for most steps. Eligibility is assessed based on your actual repayment ability and financial situation, not just whether you fit a narrow template.

To apply:

- Visit manbafinance.com and click “Apply Now”

- Enter your personal and employment details

- Upload your documents digitallyAadhaar, PAN, income proof

- Receive your approval update

- Get your loan processed and move forward

Conclusion:

Digital loan approval isn’t a featureit’s a fundamental shift in who can access credit, how fast they can access it, and how much friction stands between a financial need and the funds to address it.

For most borrowers in India in 2026, the branch-based, paper-heavy process is already behind them. The question now isn’t whether to apply digitally it’s which lender to apply with.

Check your eligibility at manbafinance.com and see how much simpler the process has become.

Frequently Asked Questions

What is a digital loan approval process?

It’s a loan application and verification system that works entirely online from application and document submission through to approval and disbursal without requiring branch visits or physical paperwork.

Are online loan approvals actually faster? Yes, meaningfully so. Processes that previously took 7–14 days with manual review now typically complete in 24–48 hours with automated verification, and some loan types offer same-day decisions for eligible applicants.

Do I need to visit a branch at any point? For most digital lenders, including Manba Finance, the vast majority of the process is remote. Some lenders may require a physical verification step depending on the loan type and amount, but this is increasingly the exception rather than the rule.

Are digital lending platforms safe to use? Established, RBI-regulated lenders use encrypted data handling and government-authenticated identity verification. The risks are primarily around fraudulent platforms impersonating real lenders that always apply through an official website and never share OTPs.

Can I apply if I’m a first-time borrower with no credit history? Yes. Digital lenders that assess income patterns and banking behaviour rather than relying solely on credit scores are often better positioned to evaluate first-time borrowers fairly.